Insights into ASX Stocks

Can Australian Mines (ASX: AUZ) Hold Its Breakout and Target Higher Levels?

Australian Mines (ASX: AUZ) is a critical minerals explorer focused on battery metals, rare earths, and gold across Australia and Brazil, advancing projects like Sconi and Flemington while leveraging strong commodity trends and strategic funding to drive its 2026 share price recovery.

Telix Pharmaceuticals (ASX: TLX) Rebounds From Heavy Sell-Off Reignites Investor Optimism

Telix Pharmaceuticals (ASX: TLX) is recovering after a sharp biotech sell-off driven by regulatory and legal concerns. Renewed investor confidence follows strong revenue growth, progress in Phase 3, and a Regeneron partnership, with FY2026 revenue nearing US$1 billion and pipeline milestones advancing.

Is Neuren Pharmaceuticals (ASX: NEU) Poised to Reclaim Higher Levels After Forming a Higher Low?

Neuren Pharmaceuticals (ASX: NEU) is a rare-disease biotech generating revenue from DAYBUE while advancing NNZ-2591. After declines from regulatory and guidance setbacks, improving US rollout and technical strength suggest a recovery, with the stock forming higher lows and testing key resistance levels.

Marmota (ASX: MEU) Share Price Surges as Traders Chase Momentum in South Australia Gold Play

Marmota (ASX: MEU) has surged back into focus after strong gains driven by high-grade drilling results from its Greenewood gold project in South Australia. Renewed exploration activity, rising gold prices, and aggressive drilling have boosted investor interest. The stock remains highly speculative but increasingly watched by ASX momentum traders.

Has Neurizon Therapeutics (ASX: NUZ) Formed a Sustainable Long-Term Floor at Its Multi-Year Support Base?

Neurizon Therapeutics (ASX: NUZ) is a clinical-stage biotech developing NUZ-001 for ALS and other neurodegenerative diseases. Despite promising data and global trials, the stock faces pressure from clinical delays, dilution, rising losses, and ongoing uncertainty typical of pre-revenue biotech companies.

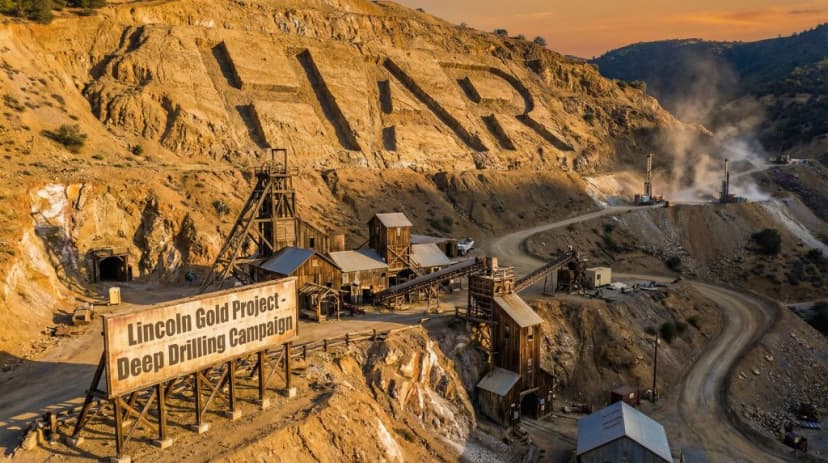

Haranga Resources (ASX: HAR) Rockets Higher as Gold Discovery Frenzy Ignites Massive Share Price Volatility

Haranga Resources has seen sharp volatility driven by renewed excitement around its Lincoln Gold Project in the US, with drilling results and expected JORC resource updates fueling speculation. The company remains an early-stage explorer, heavily dependent on exploration success, making its share price highly sensitive to news flow and gold sentiment.