Blogs

Stakk (ASX: SKK) Surges on Growth Momentum After Record Revenue Expansion

Stakk (ASX: SKK) has surged, reporting record $5.52 million in March quarter revenue and 186% growth, driven by its Stakk IQ embedded finance platform. Expanding across Australian and U.S. banks, healthcare, and regulated industries, it secured major contracts, lifting ARR toward A$26 million.

Has Tivan (ASX: TVN) Formed a Sustainable Long-Term Floor?

Tivan (ASX: TVN) develops critical minerals across Australia and Timor-Leste, led by the Speewah Fluorite project. Following a post-feasibility sell-off and rising cash burn, the stock faces a neutral-to-bearish technical outlook ahead of its late-2026 Final Investment Decision.

Is Tamboran Resources Corporation (ASX: TBN) Uptrend Still Intact Following Its Pullback to Support?

Tamboran Resources is a pre-production shale gas developer in the Beetaloo Basin, advancing toward first gas in 2026. Strong drilling results, contracts, and infrastructure progress support its uptrend, though risks remain around execution, funding, and market access beyond initial supply agreements.

Can Australian Mines (ASX: AUZ) Hold Its Breakout and Target Higher Levels?

Australian Mines (ASX: AUZ) is a critical minerals explorer focused on battery metals, rare earths, and gold across Australia and Brazil, advancing projects like Sconi and Flemington while leveraging strong commodity trends and strategic funding to drive its 2026 share price recovery.

Telix Pharmaceuticals (ASX: TLX) Rebounds From Heavy Sell-Off Reignites Investor Optimism

Telix Pharmaceuticals (ASX: TLX) is recovering after a sharp biotech sell-off driven by regulatory and legal concerns. Renewed investor confidence follows strong revenue growth, progress in Phase 3, and a Regeneron partnership, with FY2026 revenue nearing US$1 billion and pipeline milestones advancing.

Is Neuren Pharmaceuticals (ASX: NEU) Poised to Reclaim Higher Levels After Forming a Higher Low?

Neuren Pharmaceuticals (ASX: NEU) is a rare-disease biotech generating revenue from DAYBUE while advancing NNZ-2591. After declines from regulatory and guidance setbacks, improving US rollout and technical strength suggest a recovery, with the stock forming higher lows and testing key resistance levels.

Marmota (ASX: MEU) Share Price Surges as Traders Chase Momentum in South Australia Gold Play

Marmota (ASX: MEU) has surged back into focus after strong gains driven by high-grade drilling results from its Greenewood gold project in South Australia. Renewed exploration activity, rising gold prices, and aggressive drilling have boosted investor interest. The stock remains highly speculative but increasingly watched by ASX momentum traders.

Has Neurizon Therapeutics (ASX: NUZ) Formed a Sustainable Long-Term Floor at Its Multi-Year Support Base?

Neurizon Therapeutics (ASX: NUZ) is a clinical-stage biotech developing NUZ-001 for ALS and other neurodegenerative diseases. Despite promising data and global trials, the stock faces pressure from clinical delays, dilution, rising losses, and ongoing uncertainty typical of pre-revenue biotech companies.

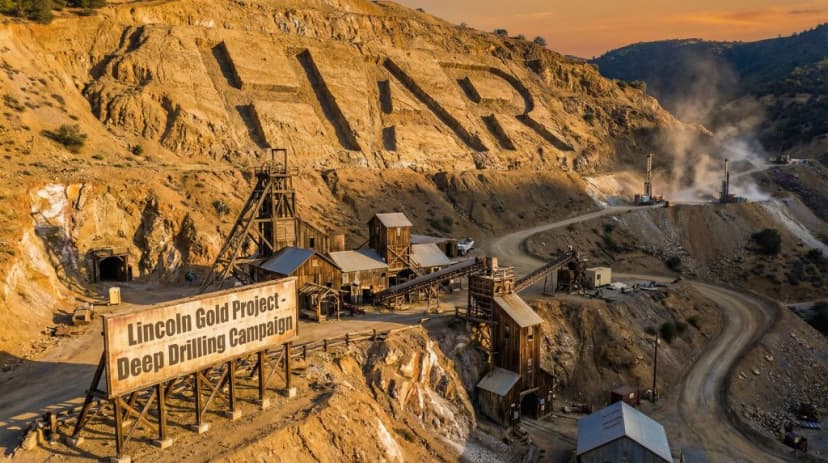

Haranga Resources (ASX: HAR) Rockets Higher as Gold Discovery Frenzy Ignites Massive Share Price Volatility

Haranga Resources has seen sharp volatility driven by renewed excitement around its Lincoln Gold Project in the US, with drilling results and expected JORC resource updates fueling speculation. The company remains an early-stage explorer, heavily dependent on exploration success, making its share price highly sensitive to news flow and gold sentiment.

Minbos Resources (ASX: MNB) Explodes Higher as Funding Breakthrough Sparks Massive Share Price Surge

Minbos Resources surged after securing US$21.5 m+ in debt funding for its Cabinda Phosphate Project in Angola, boosting investor confidence in its move toward production. The market now eyes construction progress, though execution, funding, and ramp-up risks remain significant.

Is Elevra Lithium (ASX: ELV) Ready to Break Through Key Resistance?

Elevra Lithium (ASX: ELV) is a dual-listed North American-focused producer with growth assets, led by its Québec NAL operation. Recent share moves reflect capital raising, record production, index inclusion, improving lithium sentiment, while technicals show an uptrend nearing key resistance.

Imugene (ASX: IMU) Roars Back to Life as Explosive Share Price Rebound Sparks Fresh Speculative Buzz

Imugene (ASX: IMU) surged over 35% after early Azer-cel trial results showed strong response rates in blood cancer patients, reigniting biotech speculation. Despite the rally, the stock remains highly volatile and pre-revenue, with future moves dependent on clinical progress, funding needs, and upcoming ASCO updates.

Has Galan Lithium (ASX: GLN) Built a Durable Base for Its Next Leg Higher?

Galan Lithium (ASX: GLN) is an Australian developer focused on high-grade lithium brine projects in Argentina, led by Hombre Muerto West. It is advancing toward production, supported by strong lithium prices, funding, and expansion, though dilution and execution risks remain.

ClearVue Technologies (ASX: CPV): Base-Building at Key Support, Is a Trend Reversal Finally Ahead?

ClearVue Technologies develops solar glass for energy-generating buildings. A recent Cyprus contract, improved losses, and reduced dilution sparked a bounce from key support, but the broader trend remains bearish, with confirmation of reversal dependent on stronger volume and sustained commercial traction.

Is Ionic Rare Earths (ASX: IXR) Building a New Medium Term Bullish Trend?

Ionic Rare Earths is an Australia-based company developing a vertically integrated rare earth supply chain across mining, refining, and recycling, anchored by its Makuutu project in Uganda and UK processing operations, targeting clean energy, manufacturing, and defence markets.

Clarity Pharmaceuticals (ASX: CU6) Shares Edge Higher After Investors React to Recent Price Swing

Clarity Pharmaceuticals (ASX: CU6) has seen renewed share price volatility as investors react to clinical updates and broader ASX healthcare swings. Despite pullbacks, interest in its radiopharmaceutical pipeline remains, especially SAR-bisPSMA. The company remains unprofitable, with valuation driven by trial progress and long-term oncology potential rather than current earnings.

AnteoTech (ASX: ADO) Rockets Higher as Battery Tech Breakthrough Ignites Massive Share Price Surge

AnteoTech (ASX: ADO) surged over 46% after independent validation of its Ultranode™ 95 silicon anode technology in commercial battery cells, boosting energy density. The breakthrough reignited investor interest in the speculative micro-cap amid hopes of future battery partnerships.

PolyNovo (ASX: PNV): Our Bottoming Thesis Confirmed by a Breakout Move

PolyNovo (ASX: PNV) is an advanced wound care company whose NovoSorb platform drives strong U.S.-led growth. After the March weakness from leadership changes, improving revenues and a technical breakout above the trend signal a potential bottom and renewed bullish momentum.

Nyrada (ASX: NYR) Shares Are Suddenly Back on Traders’ Radar After Sharp Price Swing

Nyrada (ASX: NYR) shares have seen sharp volatility as traders react to its Xolatryp clinical progress and Phase IIa plans. Despite strong preclinical results and early trial safety data, the stock remains speculative, driven by momentum trading, retail interest, and upcoming biotech milestones.

Aristocrat Leisure (ASX: ALL): Strong Results Spark Re-Rating—But Can Growth Continue?

Aristocrat Leisure is a global gaming company delivering strong HY26 earnings growth and driving a share price re-rating, supported by buybacks and land-based strength, while investors remain cautious about whether digital segment growth can sustain long-term momentum.

Elders (ASX: ELD) Shares Just Crashed More Than 20% as Guidance Cuts Shock Investors

Elders' shares fell over 20% after investors focused on weaker FY26 guidance, rising input and fuel costs, integration risks, despite strong half-year earnings growth driven by better conditions and Delta Agribusiness contributions, highlighting concerns about future margins and outlook uncertainty.